A (F)innovator's Dilemma

A (F)innovator's Dilemma

What happens when lending and payments collide?

If you are anything like me, you spent a number of waking hours in November glued to the national news to see… when Affirm’s S-1 would be made public, following their confidential filing last month.

Alright, that may not have been the only big story on my mind.

But I had been keeping an eye out for their filing amidst a busy month at my my real job and the occasional glance at the election. I was planning to do an S-1 analysis for Affirm (similar to he one I did for Lemonade) and figured that they might try to capitalize on the hot IPO market in November. As of this morning, their debut is on track for next month, so that analysis will have to wait. Either way, I spent a fair amount of time thinking about the Max Levchin’s “Buy Now, Pay Later” (or BNPL) behemoth.

This was in part due to the fact that, over the last month, two separate people asked me a very important question about Affirm. In fact, one person posted it as a question to my last newsletter:

Why do you think [Affirm is] NOT easily replicable by banks with access to the low cost of funds....

And this question stopped me in my tracks.

A number of years ago, when I was starting to build a basic understanding of fintech, this important financial principle was one that was made clear to me by a beloved professor. At the time, we were discussing peer-to-peer lending, which has historically been haunted by high capital costs, but the same truth holds across lending. Bank deposits are essentially the cheapest form of capital (at almost zero cost), which on its own, creates a difficult lower bound for any other lender to compete with.

So having given it some thought over the last few weeks, I saw it as an opportunity to dive into this fundamental question of financial innovation.

But before we do that…

Let’s meet the players

Before we talk about capital costs, I felt it was important to improve my understanding of how the BNPL (or POS financing) space works. Having little understanding of it up until now, I started with the basics and did some research on the three big players: Affirm, Klarna, and Afterpay.

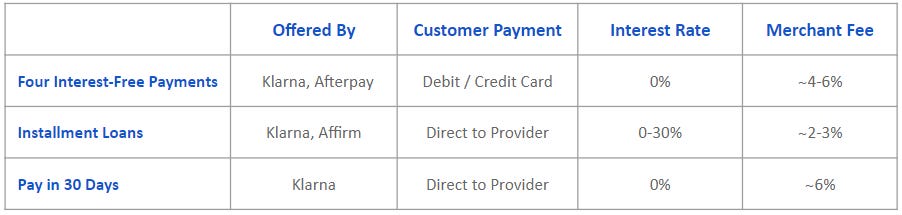

Thankfully, I was able to get a quick start from Afterpay’s great investor presentation from earlier this year. One thing I realized quickly was that there are multiple product types in this space. More specifically, although they are all loan products, these firms rely on two different revenue levers: a merchant fee and interest charged to the customer. This is easy enough to understand, but the strategic dynamics of each are very different. Here are the basics:

Two big takeaway here are that BNPL companies seem to offer either a 0% APR loans with a higher (4-6%) merchant fee OR 10-30% APR loans with a more traditional 2-3% retailer fee. In both instances they offer the merchant higher sales through increased spending and customer conversion. The consistency across firms was striking, but a little more digging led me to (at least) one more thing that I was missing: the payment method!

As it turns out, both “four interest-free payments” products differ materially from the others in that they rely on an existing credit or debit card to process the payments. This led me to a hypothesis that perhaps the product type was an important differentiator and that led me to reorganize the above table, along with some additional data:

To be honest, I’m not sure there is anything particularly new or novel about this table vs. the other one, but it did help me understand that Klarna and Affirm are the only firms with a system that bypasses the card networks (i.e. Visa and Mastercard). And it helped clarify my thinking about these product distinctions in order to address our key question:

Is BNPL easily replicable by a bank with a lower cost of capital?

With a much better understanding than I had a few weeks ago, I’m going to say “probably not.”

If we assume Klarna’s business is split evenly across its three product lines, we can estimate that the market cap for these BNPL companies is split ~70/30 between 0% APR products and 10-30% APR products. And that former 70% looks much more like a merchant acquirer than a traditional lender. Sure they have a large recurring receivable by design, but the payments for 0% APR products are due in less than 60 days. They carry some default risk, but high merchant fees and late fees provide a cushion against that. All of this creates an environment where a firm like Afterpay (who only offers 0% APR) has no need to rely on customer deposits to keep their core business profitable. You can think of them more like Square or Stripe, two huge merchant acquirers from the 21st century that have (or will) make some venture capitalists very rich because they were able to recognize this distinction.

And for the 30% of the market that charges up to (gulp) 30% APR on installment loans… the interest rate alone provides half of our answer. High interest rates make it easier to withstand a high cost of capital and companies like Affirm have clearly demonstrated that many customers prefer transparency and predictability in their payments, even if it comes in exchange for high interest rates. Remember, for a large cohort of customers, although 10-30% may sound high (and it is), their best alternative might be a credit card, which in the US carries an average APR of 15-20%, and weaker mechanisms to drive timely repayment.

One-off deals, like Affirm’s high profile 0% APR deal with Peloton, are outliers. Given the longer receivable period (39 months) and lack of interest revenue, its reasonably safe to assume that Affirm relies on some type of merchant fee and the creditworthiness of the Peloton buyer. A quick DCF analysis I put together estimates that Affirm needs to charge ~3-5% more than their organic cost of capital to turn a profit. Of course that cost of capital could vary wildly depending on how exactly Affirm funds these loans and the possibility that they take a loss on the partnership for the positive brand association. One worthy data point is that Affirm does have a lending relationship with Morgan Stanley as of 2016, which should help them keep their cost of funds down. All of the above are good things to keep an eye out on when they finally publish that S-1.

Regardless, with both products lacking a clear need for bank-deposit-cheap capital, it still begs the question: why wouldn’t a bank do this anyway? Whether or not you classify these BNPL companies as lenders or merchant acquirers, both businesses are logical fits for a traditional financial institution. Which brings us to…

The (F)innovator’s Dilemma

We’ve explored this idea before, but for those of you haven’t read Clayton Christensen’s excellent book, “The Innovator’s Dilemma,” I would highly recommend it. Like most management books, it is hardly a page turner, but Christensen truly unveils some of the mysteries around disruptive innovation in a relatively succinct manner, given the complexity of the topic. His thesis still holds up incredibly well across the board today, and especially so in financial services.

One of his key ideas, is that truly disruptive ideas, almost by definition, are impossible for incumbents to execute on. He doesn’t address exactly what the definition of “disruptive” is, but some of the things that he points to are fundamentally different unit economics, small (but quietly growing) market sizes, and development processes that require firms to create a new core competency.

There are examples all across fintech that rely on these (and more) elements of disruption. But one that sits front and center for most of them, and certainly for BNPL, is the point about development processes and core competency.

Although Affirm, Klarna, and Afterpay are certainly novel ideas, it seems to me that they have built a product that, from an external perspective, is replicable.

But the devil is in the details. Yes, these companies have created an alternative payment/lending product that is transparent for all to see, but what they have also done is hire the best product and engineering teams to build a simple integration process that makes the payment method easy for both merchant and consumer. On the other hand, the legacy systems in most banks make building such a product a non-starter. Surely any Wall Street Firm could pay top dollar for some of Silicon Valley’s finest talent, but without flexible infrastructure, it would take years to get a lesser product off the ground. During that time these firms have amassed billions of dollars in valuation.

And while I think it is important to look at each category on a case-by-case basis, I think in this instance, the focus on e-commerce makes it particularly defensible against the old guard, and a big reason why these BNPL firms have had such success. Again, I think Stripe and Square offer good comparables for similar disruption.

Of course, Christensen also concluded that M&A is corporate America’s solution to disruption. At quick glance, I don’t see any strategic investors on either Affirm’s or Klarna’s cap table and I’m not feeling bold enough to predict that a major bank will look to acquire either of them. But if it happens… you’ll know why.

Love this! We paid close attention to POS innovation in my last job where we really tried to innovate around personal lending. Another reason I think banks haven't made huge strides into POS lending is because they simply don't need to: yield-on-deposits and traditional lending provide more than enough revenue. Relative to the (supposedly) outsized sales a merchant might experience by offering a wider spectrum of payment options, the cost-benefit for a bank to develop this solution just isn't there IMO.