Fintech Exceptionalism

Fintech Exceptionalism

and how network effects can create big businesses from small ideas

“Is this a business, a product, or a feature?”

In a world where making fun of venture capitalists has become its own subculture, I realize this simple question could seem like a great place to pile on the fun.

But if you are really trying to identify the next unicorn, I’ve often found its simplicity to border on the line of elegance.

The underlying principle here is that VCs should only invest in businesses (big) as opposed to products (small) and features (tiny). We could spend plenty of time drilling into the definitions of each, but that really isn’t what we are after. The definitions themselves are finicky and many smart people have argued that the delineation is not always helpful. To be fair, they make a lot of good points.

That being said, I’ve also seen at least one smart investor use this exact logic on national television. And I can name plenty of companies that failed this basic mental test that are now in serious trouble.

Look at Casper. As of today, they are worth $275M. I’m not going to take the time and review their 10-K, but from a mile away, selling mattresses strikes me as a decent business, just not a billion-dollar one. However, at one point along the way their investors thought otherwise and the result of that discrepancy has not been pretty.

In my mind, the key here is to use this question to disqualify ideas that don’t have a plausible path to massive scale and force yourself to analyze the assumptions that are required to take an idea from feature, to product, to (big) business. The simple recognition that a Casper mattress is “just a product” could have been enough to prevent a few nightmares.

But the point here is not to highlight some of the VC misses that could have been avoided by using this gut check.

The point, as per usual, is to talk about fintech.

What sparked my inspiration for this edition was the fact that there are many exceptions to this framework in the financial technology space. And as I began to count through the number of billion-dollar products and features in the space, I realized that just one additional question to this framework can help us identify winners…

Is this a utility?

And by utility, I’m referring to the type of businesses that operate as a key node within a large, complex, network to provide a fundamental service.

The more obvious examples are the public utilities that we use daily: think of your local gas or electric provider. In a place like New York City, you could even include the MTA.

But on the private side, and specifically in finance, there are similar networks that exist in a partially digital realm. They are perfect habitats for unicorns

This is because of the sheer amount of money that moves through these complex interconnected webs creates massive opportunity. And while it may be hard to connect the nodes in the network, once you do you can create a beloved network effect.

Silicon Valley and Wall Street alike are both obsessed with network effects. The term itself has become overused and that at has left the underlying concept to be both misunderstood and overstated. Without getting too wonkish, the idea behind network effects is generally derived from some interpretation of Metcalfe’s law, stating that the power of a (telecommunications) network is proportional to the square of the number of nodes connected. In more simple terms, every user you add to a network increases the value by more than the value of just that one user.

But where Metcalfe’s law falls short when applied to other domains is in the ability to actively measure things like “power” and “cost.” This is where there are most often holes in the underlying logic of an alleged network effect. And so in order to avoid that logical trap, and go back to our “is this a utility?” question, it is important to break down a network effect into two aspects.

The first one is scalability. In a business sense, the idea here is that, as your network grows, the “power” you are building is the attractiveness of your product to other users or customers. Over time, this should accelerate your growth and dramatically lower your acquisition costs as users and customers need to be on your network to experience its benefits.

The scalability element works very well on social platforms. In the last 15 years we’ve seen MySpace, Facebook, Instagram, Snapchat, and now TikTok (or so I’ve been told) grow their user base like rocket ships in relatively short periods of time. This is simply because once the user base hits critical mass, the FOMO factor becomes real enough to attract users. Even social elements, like Robinhood’s famous refer-a friend program, can be used to achieve similar results. But as we’ve also seen over time with social platforms, they can be subject to violent swings in value with the fleeting and fickle desires of their customers.

Which brings us to the other key aspect of network effects, defensibility against competition. If you really want to achieve “utility status” and create long-term, sustainable value, this is a key piece that is often overlooked. It is driven primarily by “switching costs.” There are other reasons too, but when you have networks that are monetizing directly (i.e. the user pays for the service, as opposed to social networks that do so with ads) the network becomes more powerful in that users are less like to leave it.

A personal example from my own life is my local internet service provider. I recently received a very generous offer from a new upstart in my area that was a financial no brainer: there were offering a number of free months and a faster connection for a better monthly price. Google even told me they were legit. And yet, despite the fact that I am now working from home (making for an easy install), I didn’t switch due to some combination of the time left on my lease (10 months), a risk that the service would suck (my current provider is fine, albeit rude on the phone), and human laziness (oops). It may sound silly, but I’m sure many of you can relate, and when you aggregate all of that sentiment, you end up with a product that sticks.

And so, to bring our “utility test” back to fintech today, we will apply this lens to the payments market. As any savvy investor knows, the “we will win 1% of a $100B market” argument is underwhelming, to say the least. But when you are dealing with a a multi-trillion dollar industry like payments, it’s a different story.

Yes, that is trillion, with a “T”

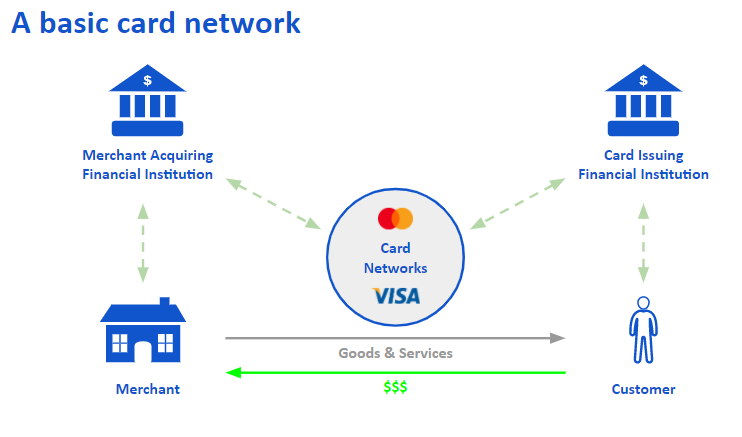

For the payments newbie, it suffices to say that the list of parties involved in your morning coffee run goes much further than you and your local barista. There are banks on both sides of the transaction that process information and some clearing parties that sit in the middle. The end result is a network that looks like this:

Worth noting, the above image is hardly original. MBA professors and industry experts use similar drawings all the time to explain the basics of payments. My intention here is not to reinvent the wheel, but rather to provide some context before diving into some specific firms.

In addition, when we talk about complexity, it is important to remember that each picture in the above diagram represents every entity in its respective category. The fact that every consumer, merchant, and bank ultimately connects to only a few credit card networks is, on its own, an incredible feat that creates high switching costs throughout the chain.

The bottom of the picture is our perspective of the transactions where, to stick with the coffee metaphor, the bright green line represents ~$4 and the grey line represents our morning cold brew (black, please). The light green dotted lines are the part we don’t always think about: the interchange fee. These fees generally total somewhere between 2-3% of the transaction and are split between my card issuer (in this case, Chase), the card network (Visa), and the financial institution used by my local coffee shop (unknown).

And now that we have a basic understanding of payments, we can talk a little bit more about the space has been disrupted by (at least) three major “products” in the last 10 years.

The first one is Stripe. Continuing with the idea that a successful fintech product needs to just carve out some space in this large network, Stripe has done exactly that, building a last reported $36B company on just seven lines of code that allow merchants to collect payments online. Today, they technically have 11 products, but they rode their payments API to their first 10 figure valuation. Was it a full-blown business back in 2010? Hardly. But it was a utility required by online merchants everywhere (and today, includes Amazon!).

The second one is Square, which in many ways is the offline equivalent of Stripe. Founded just one year before, Jack Dorsey set out to solve payment acceptance for small merchants with brick & mortar operations. You have to remember, this was only two years after the launch of the iPhone. It is hard to understate the cleverness of a card reader that plugs into an audio jack. But it was also just a product - albeit one that was filling a void in this massive market.

And so, despite their differences, Stripe & Square actually operate very similarly - both displace the “merchant acquirer” node in the payments network. The result is something that looks like this:

Technically, real payment pros consider Stripe & Square to be “payment aggregators” but we can think of function as the reasonably similar for now. And the result for these two products is a combined $100B in market capitalization.

Which brings us to our last payments disrupter for today… Affirm.

You could make the case that Affirm is not a payments company at all… but rather a lender. To that, I would say that the two need not be mutually exclusive. Throw in the fact that Affirm’s founder is one of the original founders of PayPal, Max Levchin, and it seems safe to assume that he knows a thing or two about payments.

At first glance, as a consumer, I thought of Affirm solely as an alternative payment option for consumers. But when it dawned on me that it is also an alternative for merchants, I realized that it creates an impressive opportunity to disintermediate all of middle-men we highlighted above:

Pretty clever, huh? And this single product has been reportedly valued at somewhere between $5-$10B.

Now, in this instance, I will concede that “buy now, pay later” lending would have been tough to classify as a utility in 2012. I imagine that for anybody but an ex-PayPal founder, it would have been hard to convince a venture capitalist that there was so much demand from consumers for such a product. Lucky for Max, he didn’t need the money to get started.

Either way, Affirm wedges itself in to the the massive payments ecosystem by way of the merchant. And with APRs reaching as high as 30%, they don’t need to command the type of volumes required of a traditional payments player to achieve comparable revenues. I’m sure their 0% APR deal with Peloton during the midst of a global pandemic hasn’t hurt either, but I digress.

The point here is that Stripe, Square, and Affirm were all able to attain unicorn status with products that serve as utilities for the payments network. It’s an important distinction and one that could define the difference between a small idea and a big one.

In fact, I think it is so important that we will revisit it again on a subsequent edition of “New Money.”

And until then, if you’d like some help digging deeper on this, or any other fintech topics, let me know how I can be helpful.

Thanks .. Interesting example... Regarding Affirm business model of buy now pay later. Why do you think it's NOT easily replicable by banks with access to the low cost of funds....