A banker and a VC walk into a bar...

Hypothesizing about Ribbit Capital's forthcoming SPAC

Okay, that isn’t exactly the best setup for a joke, but it did cross my mind a few weeks back when Ribbit Capital (the VC) announced that they would be launching a $600M Special Purpose Acquisition Company (or “SPAC”, a brainchild of Wall Street) .

So today, I figured we could use this as an opportunity to talk a little bit about SPACs and Ribbit Capital before making a prediction on how this SPAC could pan out.

For those of you who are unfamiliar with SPACs…

The easiest way to start de-mystifying them is to revert to their oft used moniker, “blank check companies.” In the simplest of terms, that is all they are. A SPAC is just a large pool of cash held by a shell company that is publicly listed. Then, the “blank check company,” which has no underlying operating business, uses the cash to buy (or merge with) another company, usually within two years of the SPAC’s founding.

In order to avoid going down the rabbit hole of SPACs, we will avoid almost all of the obvious SPAC questions (Who raises them? What are the pros and cons of this structure? etc.), but for those interested in learning more, Investopedia is a fine starting point. And if you want to go a even deeper, this FT article provides some historical context about their reputation, the current state of the SPAC market, and a helpful walkthrough (with great pictures) of the recent SPAC deal that made DraftKings a publicly listed company.

And for those of you unfamiliar with Ribbit…

Ribbit Capital is one of, if not the leading, fintech focused VC firms in the world. Their mission, from their website, is “to change the world of finance,” and their mantra provides a clear window into their investment thesis. As an ardent observer of fintech, I think they pretty much nail it.

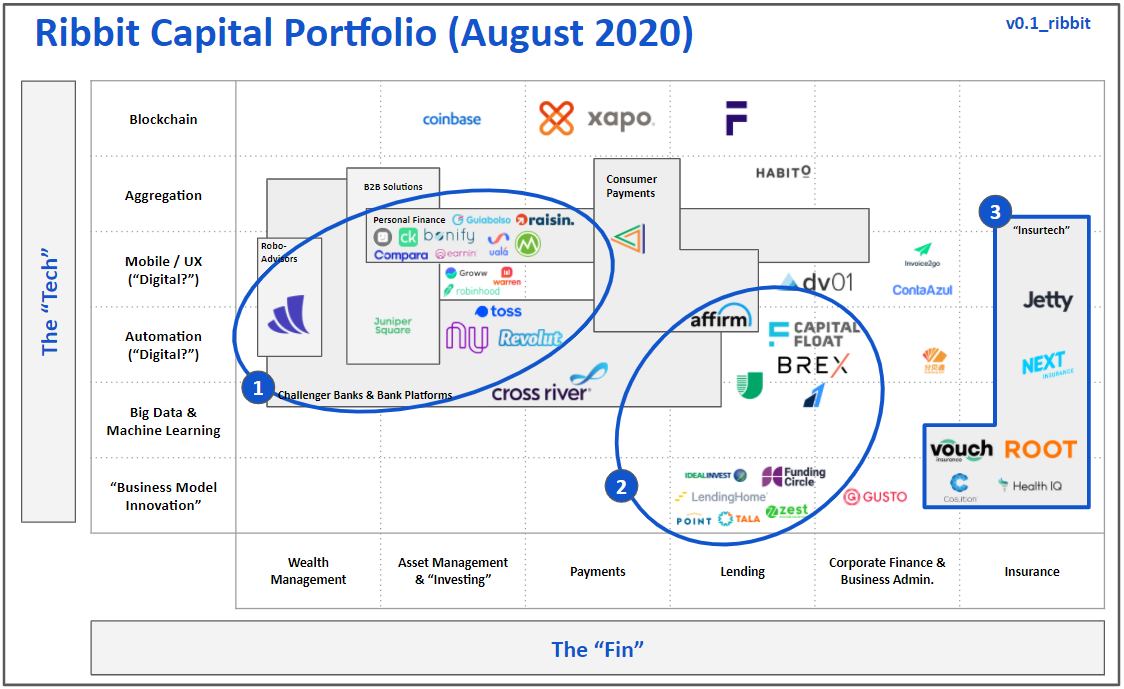

Furthermore, that thesis carries forward perfectly into their portfolio. Their investments (or “bets,” as they’ve labeled them) include an astounding number of best-in-class fintech companies across different subsectors and around the globe.

To help myself visualize their portfolio, I decided to map it on a (slightly updated) version of last week’s market map:

Needless to say, they seem to put their money where the mouth is.

Which brings us to this SPAC.

Given the possibility that a high caliber team like Ribbit may be on the verge of targeting a large fintech deal within the next two years (again, a standard SPAC search period), I found myself pondering a simple question…

Who might Ribbit target?

Which got me speculating about the conditions that might need to be satisfied by a target firm.

To be clear, like many others playing in the world of SPACs, I am definitely speculating, but this was the list I came up with:

It won’t be a company inside Ribbit’s current portfolio.

If Ribbit decided to buy one of its own portfolio companies, the conflicts of interest between the buyer (Ribbit) and seller (in this hypothetical scenario: also Ribbit) strike me as WAY too hairy to be approved from a corporate governance perspective.

Now, I might be missing something obvious here, but given Ribbit’s reputation, let’s assume they will avoid this altogether. This eliminates a relatively high number of “likely targets” given the quality of their portfolio. And if I am missing something obvious on the governance side, I’d love to hear from you.It will be a company valued at at least $600M.

Without getting TOO deep into a corporate finance lesson on SPACs, this one also seemed obvious to me at first also. Usually, (although perhaps there is nothing usual about SPACs), once a target is identified, it is common for the SPAC to utilize additional capital (often a “PIPE,” but no need to get technical) to purchase a company even larger than the initial amount raised.

I have reason to pause here as well. The aforementioned DraftKings SPAC deal was something I had never conceived: a combination IPO, reverse merger, and acquisition (oh my!). A similar deal for Ribbit could certainly violate this hypothesized condition. They could even go crazy and start consolidating a sub-sector of fintech (fun!). But again, for simplicity, let’s run with this one too.The target will align with Ribbit’s specific expertise.

Okay, duh, this one is probably most obvious. The SPAC market is chock-full of SPAC sponsors that plan to capitalize on their domain expertise to get a deal done. Billy Beane (the less handsome, real-life version of Brad Pitt in Moneyball) even launched a sports SPAC. So it seems safe to assume that Ribbit will do something similar.

And in order to visualize their expertise, we can use the map above to find clues about where Ribbit can credibly claim an edge. For me, I see three loosely defined buckets in their portfolio…

…which I’ll define as 1) “consumer finance” (broad, but workable), 2) “alternative lending” (less broad and sometimes “low tech”), and 3) “insurtech” (which is still pretty hot right now).

And then I went to Crunchbase where I turned these criteria into a filter that returned ~230 results. And because Crunchbase tags aren’t perfect, I reviewed them myself to whittle down the list of 23 companies that I would call “Likely targets for Ribbit’s potential SPAC” (catchy, I know):

Which will serve as our “prediction list” for now.

Even if 23 companies isn’t the boldest prediction, it’s a useful size to revisit if/when Ribbit de-SPACS (the process of closing the blank check transaction).

If we’re right, perhaps we will have uncovered some insight into how the team behind the deal approached it.

And if we’re wrong, we’ll have some very clear assumptions to pull apart. As is often the case in life, you can learn a lot more from failure.

Of course, Ribbit’s plan to launch a SPAC is, as far as I can tell, just that - a plan. There is a chance they don’t go through with it. Even if they do, it is possible that they never close a deal, which has happened to ~5% of SPACs in recent years.

And if you are still waiting for that punchline…

I’m going to give myself two years to finish it, and if I do, there’s a chance you could’ve predicted it anyway.